Crypto

An Overview Of The Tradeoffs For Different Sidechain Implementations

This is an opinion editorial by Shinobi, a self-taught educator in the Bitcoin space and tech-oriented Bitcoin podcast host.

This article is the last in a series diving into the major sidechain designs that exist for Bitcoin. It is highly recommended to read the preceding pieces before this: (1) Spacechains, (2) Spacechain Use Cases, (3) Softchains, (4) Drivechains, (5) Federated Chains.

What are sidechains in a nutshell? Blockchains that allow you to move your bitcoin from the Bitcoin blockchain to this other sidechain. Therein lies the issue and the difficulty with designing a sidechain — you can’t actually do that. You can’t move bitcoin from the Bitcoin blockchain to another blockchain; that’s not possible because the only place your bitcoin actually exists is on the Bitcoin blockchain. They can’t actually exist anywhere else. All that is really possible to do is to lock your bitcoin in some way on the Bitcoin blockchain and then create other tokens on a different chain to represent those bitcoin. The highest aspiration of a sidechain is to do so in a way where it is verifiable that these tokens only exist 1:1 with real bitcoin (easy), and where the only way to unlock bitcoin on the mainchain in any situation is to verifiably lock tokens you legitimately control on the other chain (very hard to do in a trustless way that doesn’t make bitcoin itself more expensive to verify).

Almost all the difficulties around designing a sidechain come down to how this locking and unlocking mechanism is designed: how locking them works, what conditions are required to unlock them and how those conditions are verified and enforced. One-way mechanisms, where you can only lock coins and never unlock them, are trivially simple. Just burn some bitcoin with OP_RETURN and require verifying that to mint tokens on the new chain and you’re done. Two-way mechanisms, supporting both locking and unlocking, are a lot more complicated. So far there is no designed two-way mechanism except ones that increase the validation cost of the main Bitcoin blockchain (softchains), or ones that introduce new trust assumptions on the security of coins locked “in the sidechain” (drivechains and federated chains).

The holy grail of sidechains is a mechanism for locking and unlocking coins that does not require any trust to enforce it, and that does not increase the validation costs of the main Bitcoin blockchain (i.e. a single sidechain interaction with the mainchain is no more expensive, give or take, to verify than a single Bitcoin transaction). Currently nothing accomplishes that, so time to go through the downsides.

Mining Centralization

All of the different designs I’ve gone through, except for Liquid, in one way or another depend on Bitcoin miners to provide security for the sidechain. RSK, even though it is a federated peg, still uses Bitcoin miners. Softchains could in theory use something else, but if it did not provide as much proof-of-work (PoW) security as Bitcoin miners, then it would be opening the Bitcoin blockchain up to denial-of-service (DoS) attacks. So, in reality, if a softchain were deployed, it would use Bitcoin miners. Spacechains PoW is based explicitly on Bitcoin miners confirming a commitment transaction for the sidechain. Drivechains are specifically designed for merge mining by Bitcoin miners. There is no escaping getting miners involved in sidechains if anything more except a pure federated sidechain is all that is ever deployed.

One clear distinction needs to be made before going into this risk: the difference between miners themselves (hardware operators) and mining coordinators (pools; the node constructing blocks). Pools are necessary to collect a reward regularly if you do not have a very significant amount of physical mining hardware and are a legitimate point of centralization. Mining centralization/decentralization is not a simple topic (more here) and there are important nuances in how different aspects of mining being centralized interact with other aspects of mining. Without mining pools, a miner’s income is a totally erratic, unpredictable revenue stream. This in, combination with the very real risk of potential regulation of mining pools in future (they are a custodial entity; they custody users’ funds until withdrawal), makes mining pools a very dangerous point of centralization for the space.

Miners have to validate the blockchain in order to mine, regardless of whether or not this function is outsourced. Without validating the chain, they have no clue whether the block they are mining contains only valid transactions; all it takes is a single invalid one to invalidate the block they find and lose them all the money they could have earned. This requirement for validation is, however, not the reason mining pools are used: it’s the predictability of rewards. A miner with 1% of the hashrate will only very rarely find a block and collect the whole reward, while a miner with 1% of the hashrate using a pool will regularly collect roughly 1% of the block reward that the pool collectively earns. The validation cost is tiny. The reward predictability is the selling point, which is why developers are trying to find a way to get those same benefits without requiring a centralized pool. This would allow miners to not depend on a centralized entity that has control over which transactions go into a block.

Now imagine if the validation costs were higher. There is no limit to the number of spacechains that can be created. And while they are not pegged to bitcoin in price like other designs, any of them that holds a significant value would be worth it for mining pools (and miners) to run in order to gain more money. Miners who did so would be more competitive than those who didn’t, and if mining in the long term becomes an industry with razor-thin profit margins, this effectively becomes a requirement to mine these other chains. If you don’t you aren’t profitable. Miners who do run them can drive costs higher for miners who don’t and still profit, driving the others out of business.

Also remember, there is no limitation on the validation costs of a sidechain. It can be very costly to validate some cryptographic functions, arbitrary complexity like Ethereum or even full-on gigablock stupidity like BSV. Softchains have the exact same risk, in addition to increasing the validation cost of regular users running full nodes. The only “saving grace,” if you want to call it that, is the requirement to activate a single sidechain at a time with a unique softfork. That at least means that each individual proposal and its validation cost will be heavily scrutinized before being activated.

Drivechains? They claim to solve this issue, but the reality is they don’t. The notion of a drivechain is that the block creator winds up paying most of the fees to miners to have their block mined, keeping only a small portion for themselves. That small portion in a world of razor-thin profit margins is more profit that can be had, which again comes back to being able to drive other miners out of business if you do it yourself. Even if you assume drivechain block creators keep none of the fees for themselves, giving 100% to miners, why would they do this if there was not some other aspect of this sidechain that they can monetize? That’s likely a form of Miner Extractable Value (MEV) that miners could make money off of, having the same centralizing effect. In the long-term, any type of decentralized mining pool would have to involve miners running all of these sidechain nodes in addition to a mainchain node, which could wind up being a very unrealistic prospect for small-scale miners. That would put an artificial floor restricting how decentralized mining could be.

Only federated sidechains avoid this centralizing effect on Bitcoin mining because they in no way interact with miners, except by virtue of paying miner fees on transactions pegging coins out of the sidechain.

The Risks Of Pegs And Consensus

The process of how sidechains are mined presents risks to mining centralization and the process of how coins are locked and unlocked from a sidechain peg can present risks to consensus. Federated pegs and one-way pegs do not present a serious risk to consensus. In the case of a federated peg, because it is fundamentally not any different than a custodial exchange — you can deposit to and withdraw from them — it does not have any fundamental interaction with the consensus process that exchanges do and so presents no new risk. One-way pegs are simply a way to burn your bitcoin and make them irrecoverable. This is not a risk or interference in consensus. Softchains and drivechains, however, both in different ways present risks to Bitcoin consensus.

Softchains present a very clear consensus risk to the main Bitcoin network. Firstly it raises the cost of validation per softchain added for mainchain-only nodes, and depending on the size of blocks or complexity of rules to validate this, can be a marginal increase or a quite drastic increase. Secondly, any consensus split due to a non-deterministic bug could affect the mainchain. Such a bug was the cause of the chainsplit that occurred in 2013. Due to how the database Bitcoin uses to handle reading and writing data works, some nodes would “run out of” times they could read and write data and invalidate an otherwise invalid block. Because these operations were limited based on individual computer resources, there was no consistent situation that would cause this, as each individual node’s resources are different.

Such an incident on a softchain presents a consensus risk to the mainchain because of how they are intertwined. Lastly, how the difficulty requirements are defined for mining a softchain can have huge implications for the validation cost of mainchain-only nodes. Any detection of a softchain chainsplit triggers downloading and validating every block down to the root of that chainsplit, which, depending on the validation costs of a specific softchain, could create a massive validation increase for mainchain nodes. If the mining difficulty is or can even be allowed to be too low of a percentage of the total Bitcoin hash rate, it could become very cheap to attack Bitcoin creating chainsplits on the softchain just to increase mainchain node costs.

Drivechains present a more subtle risk to consensus. As discussed above they do in fact have dynamics like other sidechain designs that create pressure further centralizing mining. This interacts very poorly with the fact that the peg is essentially just miners in total control of the coins in drivechains; a majority of them can effectively do whatever they want with coins locked in drivechains. The safety of all coins on drivechains depends on miners being decentralized enough to make 51% attacks not practical, but at the same time creates pressures that will likely in the long-term increase mining centralization.

If such a dynamic plays out with drivechains and miners steal coins from the peg, there is literally no option for users of that sidechain except a user-activated soft fork (UASF) to invalidate that peg out. This would be a very different dynamic than the last UASF; in 2017 users essentially played a game of chicken where they would have coins on both sides of the fork. Both options were available to people supporting a UASF. In the event of a UASF to stop drivechain theft, users would not have both options available. Only on the UASF side of the fork would they have coins; on the legacy chain they would have nothing. They literally have no incentive to come back to the legacy chain if the UASF fails and results in a chainsplit.

Some even argue that miners should attack certain “bad” sidechains (though it’s not certain what constitutes “bad” in a sidechain). If drivechains were widely adopted, this entire dynamic could fragment the Bitcoin blockchain and dilute its network effect. People victimized by a drivechain theft have every incentive in the world to keep a fork going, as letting it die means they have lost everything.

Wrap Up

It would be remiss of me to not mention federated sidechains in this piece; they do not present direct threats to Bitcoin consensus like other designs, but by their nature are effectively a trusted system. Users of such systems should consider deeply whether the utility offered by such systems are worth the trade off in security model, and whether the federation operating the system is trustworthy enough to hold custody of their funds.

In the end, no currently proposed sidechain design comes close to fulfilling the original promise of sidechains laid out in the original 2014 paper. They all either fail to provide the level of security desired in a pegging mechanism to move between chains or present risks to the main Bitcoin network itself. Maybe one day things like zero-knowledge proofs could provide a way to design a peg that does not impose increased validation costs on mainchain nodes like softchains, or not require new trust assumptions like drivechains or federated chains in terms of the security of users’ funds. But as of now, no such concrete design exists. If you think truly trustless sidechains are an important improvement for Bitcoin, hopefully one day the technology to implement them will be developed, but currently nothing in existence has come close.

This is a guest post by Shinobi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

El Salvador’s Minister of the Economy Maria Luisa Hayem Brevé submitted a digital assets issuance bill to the country’s legislative assembly, paving the way for the launch of its bitcoin-backed “volcano” bonds.

First announced one year ago today, the pioneering initiative seeks to attract capital and investors to El Salvador. It was revealed at the time the plans to issue $1 billion in bonds on the Liquid Network, a federated Bitcoin sidechain, with the proceedings of the bonds being split between a $500 million direct allocation to bitcoin and an investment of the same amount in building out energy and bitcoin mining infrastructure in the region.

A sidechain is an independent blockchain that runs parallel to another blockchain, allowing for tokens from that blockchain to be used securely in the sidechain while abiding by a different set of rules, performance requirements, and security mechanisms. Liquid is a sidechain of Bitcoin that allows bitcoin to flow between the Liquid and Bitcoin networks with a two-way peg. A representation of bitcoin used in the Liquid network is referred to as L-BTC. Its verifiably equivalent amount of BTC is managed and secured by the network’s members, called functionaries.

“Digital securities law will enable El Salvador to be the financial center of central and south America,” wrote Paolo Ardoino, CTO of cryptocurrency exchange Bitfinex, on Twitter.

Bitfinex is set to be granted a license in order to be able to process and list the bond issuance in El Salvador.

The bonds will pay a 6.5% yield and enable fast-tracked citizenship for investors. The government will share half the additional gains with investors as a Bitcoin Dividend once the original $500 million has been monetized. These dividends will be dispersed annually using Blockstream’s asset management platform.

The act of submitting the bill, which was hinted at earlier this year, kickstarts the first major milestone before the bonds can see the light of day. The next is getting it approved, which is expected to happen before Christmas, a source close to President Nayib Bukele told Bitcoin Magazine. The bill was submitted on November 17 and presented to the country’s Congress today. It is embedded in full below.

This is an opinion editorial by Joakim Book, a Research Fellow at the American Institute for Economic Research, contributor and copy editor for Bitcoin Magazine and a writer on all things money and financial history.

I don’t.

That’s it. That’s the article.

In all sincerity, that is the full message: Just don’t do it. It’s not worth it.

You’re not an excited teenager anymore, in desperate need of bragging credits or trying out your newfound wisdom. You’re not a preaching priestess with lost souls to save right before some imminent arrival of the day of reckoning. We have time.

Instead: just leave people alone. Seriously. They came to Thanksgiving dinner to relax and rejoice with family, laugh, tell stories and zone out for a day — not to be ambushed with what to them will sound like a deranged rant in some obscure topic they couldn’t care less about. Even if it’s the monetary system, which nobody understands anyway.

Get real.

If you’re not convinced of this Dale Carnegie-esque social approach, and you still naively think that your meager words in between bites can change anybody’s view on anything, here are some more serious reasons for why you don’t talk to friends and family about Bitcoin the protocol — but most certainly not bitcoin, the asset:

- Your family and friends don’t want to hear it. Move on.

- For op-sec reasons, you don’t want to draw unnecessary attention to the fact that you probably have a decent bitcoin stack. Hopefully, family and close friends should be safe enough to confide in, but people talk and that gossip can only hurt you.

- People find bitcoin interesting only when they’re ready to; everyone gets the price they deserve. Like Gigi says in “21 Lessons:”

“Bitcoin will be understood by you as soon as you are ready, and I also believe that the first fractions of a bitcoin will find you as soon as you are ready to receive them. In essence, everyone will get ₿itcoin at exactly the right time.”

It’s highly unlikely that your uncle or mother-in-law just happens to be at that stage, just when you’re about to sit down for dinner.

- Unless you can claim youth, old age or extreme poverty, there are very few people who genuinely haven’t heard of bitcoin. That means your evangelizing wouldn’t be preaching to lost, ignorant souls ready to be saved but the tired, huddled and jaded masses who could care less about the discovery that will change their societies more than the internal combustion engine, internet and Big Government combined. Big deal.

- What is the case, however, is that everyone in your prospective audience has already had a couple of touchpoints and rejected bitcoin for this or that standard FUD. It’s a scam; seems weird; it’s dead; let’s trust the central bankers, who have our best interest at heart.

No amount of FUD busting changes that impression, because nobody holds uninformed and fringe convictions for rational reasons, reasons that can be flipped by your enthusiastic arguments in-between wiping off cranberry sauce and grabbing another turkey slice. - It really is bad form to talk about money — and bitcoin is the best money there is. Be classy.

Now, I’m not saying to never ever talk about Bitcoin. We love to talk Bitcoin — that’s why we go to meetups, join Twitter Spaces, write, code, run nodes, listen to podcasts, attend conferences. People there get something about this monetary rebellion and have opted in to be part of it. Your unsuspecting family members have not; ambushing them with the wonders of multisig, the magically fast Lightning transactions or how they too really need to get on this hype train, like, yesterday, is unlikely to go down well.

However, if in the post-dinner lull on the porch someone comes to you one-on-one, whisky in hand and of an inquisitive mind, that’s a very different story. That’s personal rather than public, and it’s without the time constraints that so usually trouble us. It involves clarifying questions or doubts for somebody who is both expressively curious about the topic and available for the talk. That’s rare — cherish it, and nurture it.

Last year I wrote something about the proper role of political conversations in social settings. Since November was also election month, it’s appropriate to cite here:

“Politics, I’m starting to believe, best belongs in the closet — rebranded and brought out for the specific occasion. Or perhaps the bedroom, with those you most trust, love, and respect. Not in public, not with strangers, not with friends, and most certainly not with other people in your community. Purge it from your being as much as you possibly could, and refuse to let political issues invade the areas of our lives that we cherish; politics and political disagreements don’t belong there, and our lives are too important to let them be ruled by (mostly contrived) political disagreements.”

If anything, those words seem more true today than they even did then. And I posit to you that the same applies for bitcoin.

Everyone has some sort of impression or opinion of bitcoin — and most of them are plain wrong. But there’s nothing people love more than a savior in white armor, riding in to dispel their errors about some thing they are freshly out of fucks for. Just like politics, nobody really cares.

Leave them alone. They will find bitcoin in their own time, just like all of us did.

This is a guest post by Joakim Book. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Federico Tenga, a long time contributor to Bitcoin projects with experience as start-up founder, consultant and educator.

The term “smart contracts” predates the invention of the blockchain and Bitcoin itself. Its first mention is in a 1994 article by Nick Szabo, who defined smart contracts as a “computerized transaction protocol that executes the terms of a contract.” While by this definition Bitcoin, thanks to its scripting language, supported smart contracts from the very first block, the term was popularized only later by Ethereum promoters, who twisted the original definition as “code that is redundantly executed by all nodes in a global consensus network”

While delegating code execution to a global consensus network has advantages (e.g. it is easy to deploy unowed contracts, such as the popularly automated market makers), this design has one major flaw: lack of scalability (and privacy). If every node in a network must redundantly run the same code, the amount of code that can actually be executed without excessively increasing the cost of running a node (and thus preserving decentralization) remains scarce, meaning that only a small number of contracts can be executed.

But what if we could design a system where the terms of the contract are executed and validated only by the parties involved, rather than by all members of the network? Let us imagine the example of a company that wants to issue shares. Instead of publishing the issuance contract publicly on a global ledger and using that ledger to track all future transfers of ownership, it could simply issue the shares privately and pass to the buyers the right to further transfer them. Then, the right to transfer ownership can be passed on to each new owner as if it were an amendment to the original issuance contract. In this way, each owner can independently verify that the shares he or she received are genuine by reading the original contract and validating that all the history of amendments that moved the shares conform to the rules set forth in the original contract.

This is actually nothing new, it is indeed the same mechanism that was used to transfer property before public registers became popular. In the U.K., for example, it was not compulsory to register a property when its ownership was transferred until the ‘90s. This means that still today over 15% of land in England and Wales is unregistered. If you are buying an unregistered property, instead of checking on a registry if the seller is the true owner, you would have to verify an unbroken chain of ownership going back at least 15 years (a period considered long enough to assume that the seller has sufficient title to the property). In doing so, you must ensure that any transfer of ownership has been carried out correctly and that any mortgages used for previous transactions have been paid off in full. This model has the advantage of improved privacy over ownership, and you do not have to rely on the maintainer of the public land register. On the other hand, it makes the verification of the seller’s ownership much more complicated for the buyer.

Source: Title deed of unregistered real estate propriety

How can the transfer of unregistered properties be improved? First of all, by making it a digitized process. If there is code that can be run by a computer to verify that all the history of ownership transfers is in compliance with the original contract rules, buying and selling becomes much faster and cheaper.

Secondly, to avoid the risk of the seller double-spending their asset, a system of proof of publication must be implemented. For example, we could implement a rule that every transfer of ownership must be committed on a predefined spot of a well-known newspaper (e.g. put the hash of the transfer of ownership in the upper-right corner of the first page of the New York Times). Since you cannot place the hash of a transfer in the same place twice, this prevents double-spending attempts. However, using a famous newspaper for this purpose has some disadvantages:

- You have to buy a lot of newspapers for the verification process. Not very practical.

- Each contract needs its own space in the newspaper. Not very scalable.

- The newspaper editor can easily censor or, even worse, simulate double-spending by putting a random hash in your slot, making any potential buyer of your asset think it has been sold before, and discouraging them from buying it. Not very trustless.

For these reasons, a better place to post proof of ownership transfers needs to be found. And what better option than the Bitcoin blockchain, an already established trusted public ledger with strong incentives to keep it censorship-resistant and decentralized?

If we use Bitcoin, we should not specify a fixed place in the block where the commitment to transfer ownership must occur (e.g. in the first transaction) because, just like with the editor of the New York Times, the miner could mess with it. A better approach is to place the commitment in a predefined Bitcoin transaction, more specifically in a transaction that originates from an unspent transaction output (UTXO) to which the ownership of the asset to be issued is linked. The link between an asset and a bitcoin UTXO can occur either in the contract that issues the asset or in a subsequent transfer of ownership, each time making the target UTXO the controller of the transferred asset. In this way, we have clearly defined where the obligation to transfer ownership should be (i.e in the Bitcoin transaction originating from a particular UTXO). Anyone running a Bitcoin node can independently verify the commitments and neither the miners nor any other entity are able to censor or interfere with the asset transfer in any way.

Since on the Bitcoin blockchain we only publish a commitment of an ownership transfer, not the content of the transfer itself, the seller needs a dedicated communication channel to provide the buyer with all the proofs that the ownership transfer is valid. This could be done in a number of ways, potentially even by printing out the proofs and shipping them with a carrier pigeon, which, while a bit impractical, would still do the job. But the best option to avoid the censorship and privacy violations is establish a direct peer-to-peer encrypted communication, which compared to the pigeons also has the advantage of being easy to integrate with a software to verify the proofs received from the counterparty.

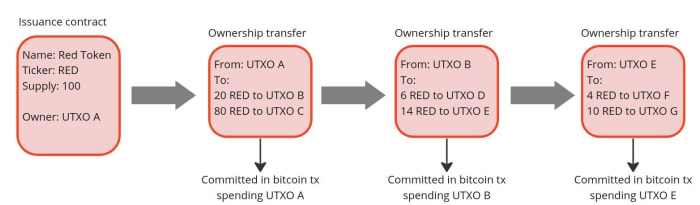

This model just described for client-side validated contracts and ownership transfers is exactly what has been implemented with the RGB protocol. With RGB, it is possible to create a contract that defines rights, assigns them to one or more existing bitcoin UTXO and specifies how their ownership can be transferred. The contract can be created starting from a template, called a “schema,” in which the creator of the contract only adjusts the parameters and ownership rights, as is done with traditional legal contracts. Currently, there are two types of schemas in RGB: one for issuing fungible tokens (RGB20) and a second for issuing collectibles (RGB21), but in the future, more schemas can be developed by anyone in a permissionless fashion without requiring changes at the protocol level.

To use a more practical example, an issuer of fungible assets (e.g. company shares, stablecoins, etc.) can use the RGB20 schema template and create a contract defining how many tokens it will issue, the name of the asset and some additional metadata associated with it. It can then define which bitcoin UTXO has the right to transfer ownership of the created tokens and assign other rights to other UTXOs, such as the right to make a secondary issuance or to renominate the asset. Each client receiving tokens created by this contract will be able to verify the content of the Genesis contract and validate that any transfer of ownership in the history of the token received has complied with the rules set out therein.

So what can we do with RGB in practice today? First and foremost, it enables the issuance and the transfer of tokenized assets with better scalability and privacy compared to any existing alternative. On the privacy side, RGB benefits from the fact that all transfer-related data is kept client-side, so a blockchain observer cannot extract any information about the user’s financial activities (it is not even possible to distinguish a bitcoin transaction containing an RGB commitment from a regular one), moreover, the receiver shares with the sender only blinded UTXO (i. e. the hash of the concatenation between the UTXO in which she wish to receive the assets and a random number) instead of the UTXO itself, so it is not possible for the payer to monitor future activities of the receiver. To further increase the privacy of users, RGB also adopts the bulletproof cryptographic mechanism to hide the amounts in the history of asset transfers, so that even future owners of assets have an obfuscated view of the financial behavior of previous holders.

In terms of scalability, RGB offers some advantages as well. First of all, most of the data is kept off-chain, as the blockchain is only used as a commitment layer, reducing the fees that need to be paid and meaning that each client only validates the transfers it is interested in instead of all the activity of a global network. Since an RGB transfer still requires a Bitcoin transaction, the fee saving may seem minimal, but when you start introducing transaction batching they can quickly become massive. Indeed, it is possible to transfer all the tokens (or, more generally, “rights”) associated with a UTXO towards an arbitrary amount of recipients with a single commitment in a single bitcoin transaction. Let’s assume you are a service provider making payouts to several users at once. With RGB, you can commit in a single Bitcoin transaction thousands of transfers to thousands of users requesting different types of assets, making the marginal cost of each single payout absolutely negligible.

Another fee-saving mechanism for issuers of low value assets is that in RGB the issuance of an asset does not require paying fees. This happens because the creation of an issuance contract does not need to be committed on the blockchain. A contract simply defines to which already existing UTXO the newly issued assets will be allocated to. So if you are an artist interested in creating collectible tokens, you can issue as many as you want for free and then only pay the bitcoin transaction fee when a buyer shows up and requests the token to be assigned to their UTXO.

Furthermore, because RGB is built on top of bitcoin transactions, it is also compatible with the Lightning Network. While it is not yet implemented at the time of writing, it will be possible to create asset-specific Lightning channels and route payments through them, similar to how it works with normal Lightning transactions.

Conclusion

RGB is a groundbreaking innovation that opens up to new use cases using a completely new paradigm, but which tools are available to use it? If you want to experiment with the core of the technology itself, you should directly try out the RGB node. If you want to build applications on top of RGB without having to deep dive into the complexity of the protocol, you can use the rgb-lib library, which provides a simple interface for developers. If you just want to try to issue and transfer assets, you can play with Iris Wallet for Android, whose code is also open source on GitHub. If you just want to learn more about RGB you can check out this list of resources.

This is a guest post by Federico Tenga. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.