Crypto

The Fed Is About To Raise Rates Again, What’s Next For The Bitcoin Price?

Watch This Episode On YouTube or Rumble

Listen To The Episode Here:

- Apple

- Spotify

- Libsyn

Transcript

[00:00:03] Q: DWill Bitcoin be Affected By Another Fed Rate Hike?ylan. We, we got a 9.1% CPI reading last week., what were your initial thoughts, reactions seeing that,

[00:00:17] Dylan: Yeah. I mean, I think it’s, inflation is, is still, is still running rampant., I think that’s, that’s mostly been, you’re starting to see the base effects of, of inflation come down a little bit, not come down, but we’ve seen commodities roll over,, in a pretty significant way., so I, I think that the, the year over year inflation could definitely have, have topped here.

I mean, I’m not a, I’m not running the data myself. I’m not, I’m not,, kind of the bureau of labor statistics. I’m not, I’m not actually calculating this stuff. ., but,, I think that,, you know what, what’s really the, the big key here is, is the labor market., that’s what the Fed’s kind of trying to squeeze out a little bit.

So inflation can still kind of like, I think you can, you can see it top out at nine, 9% or maybe it goes to 10, right. But. It’s gonna persist for a long time. There’s structural issues and, and commodity and energy markets., and, and, you know, the disinflation, the disinflationary era of the past is, is somewhat dead here.

There’s still,, kind of a lot to be worked out,, as we go forward.

[00:01:25] Q: So I just wanna remind everyone over on Twitter spaces that you will,, you’re able to see all of our pretty pre pretty faces. Jesus. I can’t talk. It’s Monday. So excuse me,, over on YouTube, we’ll be going over some charts in just a moment.

You know, look, gas prices for me have actually strangely gone down 50 cents a gallon. So I’m still sitting above $5. Like what is it in Nashville P for you and Dylan? What does it look like in Vermont?

[00:01:55] P: Man. I think,

I think for me it is just food prices. Like food prices are getting higher and higher and higher and,, it’s, it’s wild. It’s also interesting. It’s very interesting to me that, you know, I’m always fascinated by separate from what’s actually happening from how the official government narratives are shifting.

And so the more the government kind of acknowledges these increases in prices., that to me is almost a stronger signal than the actual prices themselves. So I feel like we’ve been seeing a lot more of that in terms of the public narratives that are being shilled.

[00:02:35] Q: Expand on that since you avoided the question. Sorry, Dylan. No, no. I

[00:02:39] P: was gonna say, I mean, food price is the thing for me. You said gas for gas has gone down for you, but,, you know, canceled cat food, which I eat constantly in, in order to stack more sat, save money., you know, that’s gone up and,, now h an food, obviously like, you know, fruit veggies.

I’ve just been very surprised that the, the cost, I, I ass e that has to do with fuel prices as well, but not sure.

[00:03:04] Q: Dope. Yeah. I mean, I just,

[00:03:05] Dylan: I just bought a moped, so I get 80 gallon. I had to get 80 miles a gallon. . Which you know, is great., I mean, I’m not sure about the actual gas prices. I don’t really look.,

[00:03:17] Q: but it must be nice to be that rich., all right. So let’s dive into some of these things. I., I’m with Dylan on the moped train.

I mean, to be honest, I’m looking at electric bikes myself, and then those electric bikes cost as much as used motorcycles. So I may not live to the end of this year, so I digress., we got the C CPI n bers in we’ve seen. People talking about Dr. Copper and the way copper prices are going commodities as P is meant.

Or as I mentioned, gas prices are starting to trickle down. You do see some food prices creeping up. I think it’s just a lagging effect of the high gas prices. That’s just my personal opinion though. Dylan, what are the things in the commodity space that you’re paying close attention to? Right.

[00:04:04] Dylan: Yeah, I mean, definitely looking at copper. Copper’s a really interesting relationship with inflation expectations., over the last decade, it’s like almost one for one like 10 year forward inflation expectations with, with copper., the copper to gold ratio, Lynn Alden likes to talk about it., it’s, it’s a really, if you overlay the copper gold,, ratio with, with like,, kind of industrial PMI,, you see a really, really interesting relationship there. In general commodity markets, I mean, energy, I think is, has rebounded today., we’re just in a different, we’re just in a different era, inflation. Yeah. I mean maybe the, the, the month over month of the year, over year, rate of change of inflation., can slow down, but you have to understand that in inflation compounds.

Even if inflation, you know, a year out from now is, is not 9%, but it’s 4%, you still have to take, you know, that 9% and multiply it by 4%., after that,, it’s, it’s only that kind of, that derivative,, of inflation that’s coming down. But, you know, in reality, everything’s getting more expensive over time.

I think, you know, we like to talk about just,, a big picture stuff. We we’ve our kind of thesis for, for Bitcoin., is, is kind of this asset. And obviously people say, Hey, Bitcoin’s not inflation hedge., it’s, you know, the market’s proven that in a, this Bitcoin is not a year over year CPI, cons er price, index, inflation, hedge.

But our view is that Bitcoin is a monetary to basement hedge., and when we we’re looking at kind of the, the global bond market, we still are of the belief that,, real yields over. Over the coming years will, will be,, held purposefully,, negative. Right? So, so fixed income as an asset class is guaranteed to lose you money.

Bitcoin’s obviously not doing great,, over the last, you know, year or so., but kind of, it’s still, it’s still over it’s 2020, you know, January 20, 20 opening price, whereas like the 60, 40 portfolios below that. Right. So,, I’m kind of veering all over the place here., we, we started talking about commodities,, But, yeah, I, I think that structurally commodities,, you know, we’re seeing just with the Russia, Ukraine war,, and kind of the reversal of globalization,, you’re gonna see a lot of pressure,, on, on commodity pressures for, for the long term.

But something like a recession, something like a, kind of a collapse in demand,, which the fed is trying to engineer. Those can certainly make an impact on the margin and lower those price.

[00:06:30] Q: I mean, look, we’re, we’re bouncing around a lot, but that’s due in large part because everything seems to be connected and intertwined with one another.

Look off of the heels of that CPI reading that we got last week, it seemed as though the potential for. A 75 basis point rate hike next week is actually diminishing. And the likelihood of a hundred basis point rate hike,, could be on our doorsteps. Could we talk a little bit just about where or what effect these,, the increase in fund rate could have on just the market, as we’ve seen it, as we’ve seen them progressively raise rates, we’ve seen the effect it’s had.

I mean, we’re in the midst of this bear market. What are your expectations? How are you preparing?

[00:07:16] Dylan: Yeah. I mean, the most interesting thing for me is, is that you’re seeing,, actually the, the bond markets, like calling the feds bluff,, and saying, if you look at like the eurodollar futures curve, it’s, and this is last week’s numbers.

So I couldn’t tell you exactly what they are today, but it has the fed funds rate topping out at like 3.8%, 3.9%,, this December. And then actually, if you go out to like next December,, it has the fed funds rate at, at around 3.2%., and so you’re seeing that actually the market’s expectations is that the fed actually cuts throughout 2023,, just on the basis that there’s just structurally way too much debt out there.

If you see, you know, the fed actually. Hike this, this far up, you’re gonna see kind of this, this huge collapse because of, because of how much debt there is and how much, you know, again, like the it’s a structural issue., so you kind of have this, this zoomed out view., and, and the reason why, like a lot of the Bitcoiners, or a lot of just the macro guys,, you know, despite what’s happened over the last four or five months, or, you know, what may happen the rest of the year, why they’re saying like, Hey, you know, it’s, it’s, it’s all one game and, and they’re gonna print again.

It’s. Of these, you know, big, long term structural issues of debt and demographics, which, you know, the demographic picture all over the world is, is super ugly. And so when you have these huge debt burdens and all these, kind of entitlements and promises,, that governments all over the world,, have given their citizen citizenry,, you know, it leads the, the central banks to only one,, you know, only one path, which is, which is kind of the more debate under the currency and, and, you know, printing up more IOUs to cover, to cover those promise.

[00:08:54] Q: So just for those who like me, how to quickly look up and make sure where we’re at., the current fed fund rate sits at about 1.5 to 1.7. So there’s still plenty of runway to go., . I mean, I wanna, I wanna really break this down though, Dylan and correct me if I’m wrong. If I’m ass ing that event that a lot of Bitcoiners are waiting for that reversal of the Fed’s position, this is, this would be that a decline in this federal fund implied federal fund rate would be that sometime in 20, 24, the market is expecting them to have to reverse their position.

So is that an accurate way of reading?

[00:09:34] Dylan: 2023. yeah. Oh, I mean, and you can, and you can go out and you can look at the Euro dollar features., originally Euro dollars was BEC it’s not, it has nothing to do with the Euro. It has everything to do with just the fact that European banks had dollar time deposits.

So,, Euro dollars,, the Euro dollars,, or the Euro, you know, Eurodollar futures is named after,, kind of. It was originally like offshore fed fund futures., but now that’s at the CME,, and it’s basically a way to speculate or hedge interest rates. Right. The market’s saying, you know, Hey, the Fed’s gonna raise here.

They’ve they’ve said that, but it’s gonna come down because you know, the bond market understands that it’s not sustainable over the long term., I think really what, what you,, you’re starting to see people see, and I think anyone that hasn’t read,, Arthur Hayes,, his latest piece,, I gotta, I gotta touch up on it again.

When you’re, when you’re watching, like something like the Dixie, which is a majority just kind of indexed against the Euro and the yen,, the two, you know, the second and third largest currencies in the world,, which I’ve meaningfully weakened against the dollar,, over the course of the year., because these guys are, are net energy importers, right?

So they import their energy,, and the central banks, the BOJ and the ECB are continuing their, you know, epic, monetary, monetary stimulus, right? The BOJ bank of Japan. Is kind of implementing yield curve control. They’re capping their, their bond yields at 25 basis points and the eurozone, which, you know, has, is, is super fractured and, and kind of has,, you know, weak,, weak countries within the eurozone, like, like Greece and Italy, with way too much debt to GDP.

They’re, they’re having to cap spreads, right? So the bond yields of those countries because of default risk is a lot higher than Germany. Even though Germany’s in a really tough spot with all the Russia dynamics. So they’re having to come in and actually to, you know, cap those spreads, which is another form of just money printing or quantitative easing, or maybe even yield curve control.

I think they’re calling it like some anti-fragmentation, fragmentation or something like that along those lines. But essentially you have this kind of,, you know, the second and third largest central banks are., implementing some kind of monetary policy, gone mad, while the Fed’s tightening. So you’re seeing the dollar index, which is again, just dollar relative to others, to other Fiats, mainly the euro and the yen, is soaring showing dollar strength.

And traditionally just, you know, if we go back to the history of, of this kind of this, you know, global monetary system, global monetary order. Of the dollar it’s, you know, basically post Brett and woods, or if you wanna look at it post,, you know, post Nixon shock, right? When it’s pure free flow Fiat, it’s periods of dollar strength have, have coincided with, with large global recessions.

And there’s a reason for that. It’s because there’s, there’s so much dollar denominated debt out there., so now we’re, you know, seeing that relative dollar strength, and even though the dollar,, is, is materially weakening against, you know, commodities, real goods and services., it’s, it’s strengthening against other currencies and, and this is kind of where you see like large debt crises emerge, right?

So, you know, anybody, any emerging market, whether, you know, whether it’s a European company or, or just kind of,, foreign entities, right? If they have dollar denominated debt, they have to sell dollar assets. That could be treasuries. That could be us equities. That could be Bitcoin, even right. Like anything that’s, that’s got a dollar exchange rate.

They have to sell those assets to cover their dollar liabilities. You’re essentially seeing like a short squeeze,, start to play out,, on the dollar itself., so that’s, that’s why,, dollar strength coincides with recessions and oftentimes, you know, just with, with how much,, dollar debt is out there.

And the, and the crazy thing is it’s not quantifiable., there’s, there’s, there’s so much it’s called like, you know, Euro dollars, right? Nobody knows the size of the Euro dollar market. Nobody knows how much actual dollar debt is out. It’s very opaque. And so, you know, we, we can see these, these really scary moments where the dollar just screams higher and risk sells off.

And, and actually, if we look back to like, say March of 20. You saw like the, the largest market in the world, the treasury market, it went, it was a liquid, it went no bid,, on, on one of the securities because,, there were so many foreigners that were selling treasuries to cover that, that dollar,, that dollar short position, right.

Dollar short, meaning just, dollar denominated debt. So these are like big picture issues here, but this is what, you know, a strong dollar. Why, why pay attention to the Dixie at., this is why it’s, because, you know, we have these, these huge issues that have, that have built up across decades, that, you know, are systemic.

[00:14:10] Q: I wanna quickly go back to the chart of the Dixie. Chris, if you don’t mind pulling that up and everyone who’s tuning in on Twitter spaces, just a reminder,, we have pinned to the top. You can pop on over to YouTube where you can actually see our pretty faces and the chart that I’m referencing right now.

I’m just, we’re speculating for a moment. So bear with me, Dylan, but. Are your expectations that the Dixie has peaked or is there still room for it to continue to rip higher?, historically it looks like, you know, the peak of 20 2002 or the peak in 1985 would imply we still have a good amount of runway still to go, but there could also just be an arg ent to be made that each peak has muted itself and become less and less severe.

So curious if you think the Dixie has peaked or what those expectations may be.

[00:14:58] Dylan: Yeah. I mean, okay. Like I’m, I’m not a Ford,, currency trader, like I’m not, you know, I’m not, I’m not trading dollar dollar year end dollar Euro., but just kind of as, as an outside observer of these markets,, and just, and just like, you know, looking at the structural issues of these other markets,, nevermind the fact that the Fed’s saying, Hey, we’re tightening while these other central banks are saying, you know, we’re, we’re still printing.

We’re still monetizing debt. The problem of these, these countries being net importers of energy, the structural energy,, deficit that, that the world is, is experiencing., you know, just today, this morning, Russia, like, gas prow said, said, Hey, we’re not gonna be sending Germany any more gas.

Right? There’s, you know, Germany Europe’s factory, and kind of like the, the biggest driver of the European economy, is, has a huge energy deficit that can’t be just like, just, just fixed with a, you know, with another kind of band aid, right? There’s no, there’s no easy way to fix this. So,, the weakness that you’re seeing in the Euro, the weakness that you’re seeing with other currencies relative to the dollar, nevermind the fact that the dollar,, is kind of strengthening as the Fed is supposedly going to try to.

Rollback and, and lower its balance sheet., you know, these dynamics are on change. So we’re seeing a little bit of a relief today. The Dixie’s down, I think around 1%,, which is like these moves that we’re seeing in currency markets are, are really, really big. Like these are huge, these are huge moves.

But I don’t think it’s stopped. Right., we, we actually, I think if you, if you wanna go to Bitcoin Magazine Pro, I’m trying to, trying to find out my Twitter feed right now to link., but we talked last week a little bit about,, kind of the Plaza accord,, in, in 1980s. And this was following kind of,,, Paul Volker,, raising interest rates 20%,, you know, kind of reigning in that domestic inflation that that was the United States experience in seventies, trying to, to stop the stagflationary environment.

You saw on the back of that, the dollar strengthened, significantly against a basket of other currencies. And so the world came together because as the us kind of, as the, as the dollar screened higher, the us started to have a huge, a huge deficit, a huge current account,, deficit. And so the world came together and was like, Hey, we gotta fix this.

This is, this is not ideal., this is the kind of the classic tri andous dilemma, right?, as, as the dollar gains strength,, the us just buys at the world stuff. This is, this is like a structural issue, but,, this is, you know, we’re still seeing this stuff today., the world, if the us, if the dollar strengthens too much against these other currencies, big, big problems arise.

And so, you know, the Plaza accord was essentially all these world leaders coming together and saying, Hey, we need to, we need to actually materially weaken the dollar,, and do something about this because you know, the global economy can’t function. This. And so, you know, maybe we see some sort of Plaza cord 2.0,, whether it’s, you know, explicitly or implicitly.

But you know, the longer that the dollars, the dollars up here or the higher, it goes,, the more and more problems, whether it’s under the surface or not,, you know, that the global economy will face.

[00:18:05] Q: I wanna pop on over to slide five because knowing me, I’m int misinterpreting this,, this is the us balance on current account percent of GDP. Walk us through what you’re seeing here.

[00:18:20] Dylan: Yeah. So current account,, deficit or surplus,, it’s basically how much you export or import., and so if you, if you kind of normalize it against the country’s GDP and this is for the us, right., but you’re seeing essentially,, the us being the world reserve currency, and this is something that Robert Trifon saw in the sixties.

So like anybody that’s the world reserve currency. Any country is going to have to basically run deficits to supply the world with liquidity., and if they, and if you don’t run deficits, then the world will face a recession. And so he saw, he saw this Robert Trien, an economist, he saw this in the sixties.

Essentially if you kind of, if you look at periods of, of significant,, dollar dollar strength,, this problem, this problem gets a lot worse. So now you’re kind of seeing,, our current account deficit that the strong dollar actually, while it’s, you know, kind of over a short term, could, can be a good thing as the us can, you know, buy up everyone else’s exports and, and, you know, buy the world’s goods,, for cheap.

It hollows out the, the, kind of the, the U.S. manufacturing, domestic manufacturing base and leads to a hyper financialization of our economy and, actually let’s foreigners because we’re supplying all of our dollars for the rest of the world and going into debt., it allows foreigners to, to scoop up all of our, our kind of domestic assets.

So this is, this is kind of the long term problem of, of the dollar as a world reserve currency, and why over the short term, it may be a good thing because your, your local currency, the us, you know, domestically the dollar,, is a world, is a world., you know, currency is a, is a unit of account., it’s a good thing over the short term, but over the long term, it shows the seeds for these really, really big structural issues that continue to get worse over time. And so, you know, right now it’s like five, four and half percent of our GDP is run as a deficit, our current account deficit. We import that much more than we export, and over time, that continues to kind of worsen as the tribe.

[00:20:27] Q: So it sounds like based on this chart and what we’re seeing, where we in the us are having a harder and harder time getting foreign nationals to buy what our goods are., it sounds very, very promising for the future of,, our economy and the dollar,, I want to pop on over to slide n ber seven, because actually you sent a tweet out and put this chart on my radar last week, Dylan,, just almost mocking what is actually happening,, based on what the fed is trying to tell people and the results of the CPI print.

This red yield below INFR inflation zone has now drastically spread., why should anyone be concerned about this? Like, what are, what are you seeing. .

[00:21:13] Dylan: Yeah, I mean, this is, this is for anyone that’s not looking at the chart. It’s just us CPI year over year,, and the 10 year treasury yield., and, and what it’s meant to show is,, is kind of since 1981,, since interest rates, topped,, and, and Voker got inflation under control, there’s been this, this 40 year secular trend of, of, you know,, real yield bull market in bonds.

Inflation was below bond yield. And if you have obviously like the long dated debt like bonds,, not, not treasury notes or treasury bills,, as, as the yields go down due to the duration of that debt,, the, the, the value of that debt continues to rise. So you saw this huge, huge secular bond bull market from the 1980s to 1981 to, you know, really 20, 20 or 2021.

I think, I think in 2020 was the year that the real, you know, real bond bull market ended,, just based on just based on inflation,, and, and,, where bond yields are., and so now, you know, we’re kind of seeing,, whether it’s, you know, some people there’s still bond bulls out there that think that this is just kind of a deviation.

But I’m of the opinion that this we’ve kind of seen. The top,,, of the real bull market in bonds. And so now,, whether, you know, the treasury 10-year Treasury is floating around 3%. I don’t know what it is. That’s exactly off the top of my head., you know, year-over-year inflation at 9%.

Again, even if that comes back to say 4%, 5%, you still have a, you know, we’re still witnessing financial. Reion where interest rates need to be materially lower than inflation,, to kind of erode the real value of this debt,, federal debt of GDPs over a hundred. You have debt problems all over the world.

As a fixed income holder, you’re kind of, I mean, you can, you can speculate on bonds, right? And if interest rates go lower, then you, you know, you can get a capital gain on those bonds, but just, just, kind of looking at debt as an asset class,, post 2020 post COVID potentially,, kind.

Seeing this, this huge trend of globalization that we’ve seen over the last, you know, four or five decades, but really, you know, over the last few decades with the rats of China and kind of exporting all this labor to emerging markets. We saw this huge disinflationary period,, which now,, you know, a lot smarter people than myself,, have said, Hey, this is all reversing.

The work of like Peter Zion,, Lynn Alden has written a bunch about it., if we see this period of globalization, you know, where, where everything got cheaper,, labor,, goods and services, all this stuff got, got tremendously cheap., and it’s now reversing and, and you’re seeing a lot of nations kind of become,, protectionist with their, with their trade.

And with their, with their exports,, then this, then this period of kind of inflation below yields,, is, is dead. Right? And so for a fixed income holder, you kinda have to question,, you know, your long term allocation to the asset class,, and, and, you know, wonder what your, your real returns are gonna be over the next decade or two.

[00:24:20] Q: Neither of us are experts in this space, but I just love your opinion as someone who spent far more time than I have really dissecting and looking at these things, Chris, if you could pull that chart back up. I think something that I find really interesting about this is during the. 2007, 2008 financial crisis.

You actually see the CPI print get negative, and we had a deflationary period for some time that gave the yields, this appearance of being very strong for a little bit of time., why have you just, and your research and the time you spent looking at these types of markets,, why have we not seen that?

Yet, or will we see something like that?, materialize if and when more bonds start to deteriorate?

[00:25:09] Dylan: Yeah, I mean, I, I don’t think it’s a bond market., I don’t think it’s a bond market phenomenon, I think,, basically you saw deflationary Boston in the great financial crisis., and so that’s certainly possible.

I think maybe for a brief period of time,, you know, a couple months out say, you know, if you just look at a lot of the commodity price, The year over year charts,, it’s certainly possible to get kind of a quick deflationary impulse or a negative year over year CPI reading. I certainly don’t think it’s, it’s, it’s likely,, over the short term.

That would be kind of,, that would be something where the fed would, would come in and, you know, that’s deflation is, is certainly not a, is not something that’s good for a, a credit based monetary. And so that’s why they kind of always target low inflation n bers. I mean, 2% is, is very arbitrary.

But in a Fiat credit system,,, deflationary busts are, are deadly. Right? So that’s why,, it’s just, it’s, it’s horrible for the, for the economy. And it’s why in general, when people talk about Bitcoin, this is kind of a side tangent. You say, you know, people will say deflationary money can’t work.

They’re thinking more so of a kind of credit contraction and a fractional based monetary system and not technological deflation, reducing prices,, which are two different things, in my opinion. And I think the, the, the fractional reserve credit contraction is what can oftentimes lead to this, you know,, CPI going year, year going negative.

Right., imagine like what we just saw in the Bitcoin space, right., or the crypto space broadly. Where,, you know, all these promises and all this unsecured credit blew up, we have no lender of last resort. So exchange rates, tank,, you know, say just kind of map that out to the great financial crisis where it’s not, it’s not Bitcoin or crypto markets.

It’s housing and mortgage backed securities and, and the banking system, right? You see this huge deflationary impulse and all this fractional reserve,, promises collapsing on each. And, and all these asset prices, tanking, and, and you, you see demand for goods and services fall.

And so, you know, prices on a year, year, basis contract, right? So the government comes in and injects the system with a bunch of more liquidity to keep it all propped up., and Bitcoin, we don’t have that lender of last resort, but that’s the kind of the ultimator, of a, of a Fiat monetary. Space or Fiat monetary system is that when you see the kind of fractional house of cards start to crumble, they come back in to, to, you know, to, to try to prop it back up because,, that’s kind of a, a reflexive doom loop,, when that starts to take place.

And so, you know, they, the fed, I think for the longest time wanted inflation, they didn’t want inflation this high. But, you know, a year over year as negative CPIs is certainly not something that they want either. And I think arguably you could say it’s actually probably worse,, from, from what they’re trying to achieve.

[00:28:01] Q: So you’ve now let’s, let’s, let’s go down the Bitcoin of it all., as everyone who is listening in on Twitter spaces should be aware if they’re not,, Bitcoin is in a bear market. The global economies are in a bear market, and Bitcoin has never really been alive during a global recession. We are not technically there.

And by technically I just mean the powers that get to determine whether or not we’re in a recession have just not officially come out and said that,, I wanna just. You know me, I like to speculate. I know how much you don’t like it. Just bear with me. You’re on, you’re on for the next 20 minutes. So you’re kind of stuck.

Sorry, Dylan, should the reading come out in the next, I believe it’s next week. We’ll get Q two’s GDP reading. And should we get a negative GDP reading for the second quarter? That’ll be two successive quarters. I E a technical recession will be triggered. do you think that the market is gonna be surprised by that?

And I’m talking about the general market first and then secondarily, do you think Bitcoin will be surprised by that? And by that, I mean, the price of Bitcoin?

[00:29:12] Dylan:, no, I mean, I don’t think the technical definition matters., I think just, I, I,, am of the opinion that, and it certainly would love to be proven wrong here as a, as a, you know, a large holder of, of Bitcoin.

But I, I don’t think that the bottom is, is in, and maybe we, you know, we, or maybe, maybe that’s, you know, 17, five or whatever it was for Bitcoin,, is, is a generational low and would, would love for that to be the case., certainly there was an absolute truck load of, for selling that took place,, on the back of the three arrows capital liquidation and all the, you know, the counterparty risks that resulted from.

You know, and, and before that Luna as well, right? Just like, you know, hundreds of, thousands of Bitcoin were, were puked up in, in this,, kind of event. But,, if you just kind of take a step back and look at Bitcoin as just kind of another asset,, riding the liquidity tide., I think we’re what we’ve seen since,, November.

Or maybe if, if you look at like S&P since like January, since the market’s topped,, what you’ve seen is, is that the draw down the, the bear market equities has been about duration, right? So you’ve seen yields sore., and, and because of that, the, the duration assets, which Bitcoin is, is, you know, despite having no cash flow is paradoxically treated as a long duration.

Right. So, so bonds, equities,, specifically. Right., as yields have risen,, the discount,, the discounted kind of cash flow or the, the value of these, these equities,, as the yields have risen as the risk free rate has, has soared,, the, the kind of the, the future or the valuations of these companies and, and, or these assets have, have collapsed.

You’ve seen, you know, like say like,, I think treasury bonds have the worst start of the year,, in recorded history since like the 18 hundreds, which is somewhat of a crazy stat, right? So that’s like the first leg of this bear market., and I, I kind of was, was speculating and saying, Hey, like, I, I think if, if this is to get materially worse, if we are it, you know, amidst the recession, if the fed continues to, to hike,, and you know, we see nine, 10% inflation year over year, cons ers are really starting to feel it in their pockets.

You’re seeing European, you know, that the Eurozone is getting decimated,, because of. Right. It’s we, we could expect,, or should expect some form of, of earnings, right recession. So we’ve seen the duration,, part of the decline, get really rapidly priced in. And I think for the most part that’s done, right.

Not talking about Bitcoin, but equity markets specifically, the next kind of leg. I would suspect if we are in a, in a true recession, in a true bear market., and again, you know, could be wrong here and, and the market’s been chopping around for a month as, as you know, people are trying to price all of this in, but,, traditionally what you would expect next is, is for the, is for the, kind of the earnings recession to be priced in.

So we’ve seen the duration, but I, you would expect that the EPS,, you know, revisions start to go lower., and, and, you know, if we are kind of seeing actual quantitative tightening, you’re gonna see,, credit. Start to credit risks, start to get priced in, into, into both bonds, corporate bonds and to equities.

And so,, when I think of Bitcoin, I just kind of,, another asset riding the liquidity tide, even though there is kind of,, its own exogenous variables. There is, you know, Bitcoin native derivative markets,, and certainly, you know, kind of the bounce we’ve seen Bitcoins trading at like 21, 21 6 right now, 21 7.

There’s, you know, derivative market dislocations that can, can get worked out. Dick Bitcoin’s been basically chopping around and it’s just derivative markets that have, have been sending it from 19 to 22 and back ping, ping pong back and forth for the last month or two., but if we are truly, you know, kind of in this,, global recession,, you know, potentially depression, right?

When you, when you just kind of. Quantify the energy deficit., there’s, there’s a whole lot of pain,, that that’s being felt out there., then I think, you know, the next leg lower for equities and the next kind of catalyst,, for risk off is that you see, you see these, these earning provisions really start to get hit.

And you’re seeing like, you know, people a lot smarter than myself, a lot more successful than myself. Like Michael Berry say that as well, right? He’s saying, Hey, the first leg was, was about duration and that was priced in very rapidly. But this bear market isn’t over,, and, and really you haven’t even seen the start of, of these earning downgrades and equity markets.

And so, you know, Bitcoin obviously seen a ton of for selling,, you know, derivative markets you saw, you saw a huge rise,, in, in open interest in BTC and Heath., but really, you know, and so, so you’re seeing like, I, that tells me a lot of people came in late and, and short hedged near the lows, which is, which is good thing, right.

Late shorts,, you know, are, are buyers eventually, but. And, you know, big butt, but really what you have to look out for is, is, you know, if there’s another leg lower in equities,, it’s, it’s highly, highly, highly unlikely that Bitcoin just magically. You know, is, is isolated and all of a sudden in the vacuand, and not kind of,, tied in as a, as a beta asset, like it’s been for the last six to eight months,, or really, you know, since, since March of 2020, it’s kind of just, it’s just,, a higher beta asset to, to the, you know, to, to the liquidity tied of, of the central bank, monetary policy.

And that’s not necessarily a bad thing. I think that’s, that’s actually a pretty natural progression., and that’s, you know, kind of always how big Bitcoin is gonna monetize, but that’s just my. That’s just my opinion. Someone said someone commented depression, boy,, depression now, boy. Oh boy. I don’t know about depression, but it’s certainly not looking.

I mean, I think,, the powers that we may try to avoid the word depression for as long as h anly possible until we’re so stuck deep in it, if we ever do reach that point., look, I love throwing out terms like bear market, cuz I’m a smooth brain trader like that,, in this short term window and the pullback that we’ve seen in Bitcoin.

Do you think that Bitcoin is in a bear market right now? Or do you think. This could be a moment where we’re gonna start to see that separation from the general market.

We’re 75% off the highest. My brother this certainly isn’t a bull market., not with that attitude. Yeah. I mean, if this is the lows and great, you know, and,, you know, I’ll happily,, I’ll happily, you know, ride that, ride that up.

But, I, I don’t think we’re outta the woods yet., would be happy to be wrong. I mean, you’re seeing like a lot of, a lot of, kind of under the surface acc ulation. Right. But Bitcoin is like as an absolutely scarce asset,, and very, you know, in elastic, right. It’s it’s supply and elastic relative to demand.

It’s only a couple hundred thousand Bitcoin can send the market up, up or down. Right. So prices set at the margin., and if you just think about marginal buyers versus marginal sellers, obviously the last six months have brought a ton of just indiscriminate selling., but when you’re looking at the marginal buyer,, the pledges are certainly buying.

But if you think about the average PLE or the average market participant that has no Bitcoin exposure,, traditional legacy funds are risk off, they risk adverse, and they certainly don’t wanna be speculating on an 80 vol asset. Maybe a little bit of exposure here, there dipping their toe in right legacy participants.

I think with a new basal, requirements or the new basal, What is it called regulations? You know, banks can have 1% of their assets in Bitcoin now, which is great. I don’t expect, you know, banks to come, just start Aing into Bitcoin right away., but that’s, that’s good news., the, the, kind of the, the gap,, earnings,, accounting is the gap accounting,, for corporates is still very,, is, is just not ideal.

Right? So, mark-to-market losses,, but not mark to market gains., so, you know, if you buy Bitcoin at 20 K and it goes to 10 K, you have to, you have to take a hit on your earnings. Like you’ve seen that with MicroStrategy, so that’s still not ideal., and just in general, like I, and I’ve said this on previous streams and, and not to be pessimistic,, but.

In the crypto space broadly and Bitcoin’s obviously not isolated from it. This, this last two and a half months has been a huge black eye., and so really kind of any, any participants,, serious participants that, that, you know, would wanna get involved,, you know, have, have a whole lot to kind of sort through,, following this aftermath and.

There’s kind of a lot of just, you know, opaqueness that, that people maybe previously didn’t didn’t think was out there., so, you know, I think we’ll obviously Bitcoin, we’ll get to the other side of this and, and it’s still,, a legitimate macro asset, but just in terms of, you know, the start of a new bull market coming to coming forth,, and, and, you know, all time highs by, you know, whenever, it’s I think people should just, you know, taper their expectations a little bit because we still have some, some kind.

Clunkiness to sort through from the macro perspective. And also just from a, from a regulatory perspective, like I’m, I’m not one to call for regulations. And I, I certainly don’t like big government, but just in terms of sophisticated market participants, getting involved in this space,, the last two months have certainly not been,, you know,, advantageous to, to the effort there.

[00:38:29] P: Wait, but do you think, are you saying that that is related to regulation and that regulation would help there?

[00:38:35] Dylan:, I mean, you know, I, I I’m a little conflicted because you know, part of the, the, you know, ANCO capitalist libertarian in me says, you know, abolish S sec, not actually calling for abolishing SCC, but like, you know, I, I do have that, that,, that libertarian kind of free market mindset.

But at the same time you have legitimate fraudsters, like Celsius and Alex Masinsky. And, and it looks like a lot of the three arrow stuff. And, and the whole Luna debacle. And, you know, whether that’s a legitimate, honest effort at something,, unique or not,, is another debate, but just all of this has, you know, kind of, and, and also like the, the kind of the dollar,, the dollar banks, right.

That weren’t actually, you know, these, these kind of,, digital banks that weren’t actually banks and they were just. Aping the Treasuries into UST. Right? All of this stuff is, is, basically begging regulators to come in and, and,, and enforce,, with a, with a heavier hand. Right. So,, I don’t know if it would’ve stopped it or not.

I don’t know if the S sec didn’t do its job. Good enough. Like, I, I certainly am not calling for garyinsler to, to regulate more., but I just think. It’d be foolish to think that more regulation isn’t coming on the other side of, of, you know, the craziness of the last two months, unfortunately, or fortunately.

[00:39:57] Q: Okay. So we’re gonna abolish the S E C., what about the fed? Do you wanna get rid of the fed ?

[00:40:04] Dylan: I think eventually, I expect Bitcoin out outlast the fed , but we’re not there yet. We’re just, it’s just,, you know, that’s the reality. I mean, you can certainly abolish, abolish the fed with your own full note and audit your monetary policy.

But in terms of the Bitcoin exchange rate,, you know, that is most definitely not isolated from the actions of the fed,, and it would be foolish to think otherwise.

[00:40:27] Q: So I wanna show on slide n ber 10, the. Bitcoin and Dixie year over year change chart., this, I found super, super fascinating where it almost seemed as though the peaks in Bitcoin, when it was reaching all times, highs was actually correlated with when the Dixie was making new lows.

Let’s talk a little bit about that. What does that actually mean? And could the value of Bitcoin really be derived almost in the same way where. As earlier we talked about the Dxy, it’s not necessarily that the dollar was getting stronger. It was just all these other currencies that were measured against the dollar that were getting weaker in the same way, the dollar, which all of us are in the U.S. and American.

So excuse and forgive me to any of our foreigner, viewers and guests., this reads to me like the Bitcoin price was actually driven more by dollar weakness than anything else. Is that a fair conclusion?

[00:41:26] Dylan: No, I mean, I wouldn’t, I wouldn’t say that. I mean, obviously Bitcoin,, has its own kind of adoption cycles and waves, but I think,, certainly the, the cycles and, and the, the kind of the monetization bubbles, if you will, of Bitcoin are aided by easy credit,, and, and kind of,, these, these credit cycles. So dollar weakness,, is kind of,, traditionally, or if you just look at like the past, you know, decade or. Has been accompanied with,, these kind of,,, kind of upswings and growth and credit cycles,, and easy monetary policy. And so kind of when money’s easy, when money’s cheap, you’re gonna see.

And basically that’s, you know, it’s just like liquidity is, is very available., you know, Bitcoin crypto sees a, you know, kind of a huge upswing and, and kind of,, a new, I don’t know, a, a new cycle. Right. And so, and, and when conversely, when the dollar is strengthening,, and, and you see global liquidity pulling back,, and you know, a deceleration of credit growth, or even an outright contraction of credit growth,, you’re gonna see stuff.

Crypto like Bitcoin,, you know, takes a big hit, right? So if you look at, I like to just like the last two years,, because I think Bitcoin is, even though it’s still very immature, I think it’s matured a lot more than it’s, you know, 20 15, 20 16, 20 17,, cycle., if you look at the last two years of, of Dixie and BTC,, and inverse the charts and throw BTC in log scale,, just to see a little better.

It’s like pretty, pretty similar chart., and so I think that’s certainly telling,, and obviously, you know, the dollar can, can strengthen,, or, or weaken and, and those foreign currencies kind as well., there’s, there’s a bunch of variables there,, but you know, the dollar rules, all,, which is, which is why it’s, it’s such a significant chart and why I, I pay attention to it.

[00:43:19] Q: So the dollar will rain Supreme for some time, what are some events that you are keeping an eye on that will further weaken the dollar?

[00:43:29] Dylan: Personally I’m of the opinion., and this is, you know, I’m not expecting an imminent pivot and monetary policy. I think,, you know, anybody that’s kind of, you’ve been expecting to pivot every month of 2020, then you’ve gotten your shirt ripped off.

I mean, long term investors are, you know, unbothered. And I think that in the long term. Investment thesis of BTC is completely unchanged and, you know, potentially even strengthened,, through all of this craziness., but,, really I’m of the opinion that this, and, and at what level, and at what scale is, is anybody’s guess, I certainly don’t know, but I’m of the opinion that all of this craziness leads inevitably to the,, to the fed, turning to yield curve control in some form.

So whether that’s, you know, monetizing the, you know, treasuries at at 3%, Or, you know, 2% or 0%., I I’ve, I mean, we’ve seen interest rate policy,, you know, as a tool,, be used by the fed until the great financial crisis where quantitative easing became the primary tool., now, you know, post COVID, they, you know, QE, infinity, they monetize corporate debt.

Inflation’s raging. So they’re, they’re, you know, they’re having to try to walk that back. But I think inevitably whether it’s something in the Euro dollar system,, you know, whether it’s something in international markets, Maybe the, the legacy,, or the, you know, the, the banking system, although that’s, you know, from what I, from what I see, and from what I hear from other smart people is a lot stronger than, than the great financial crisis.

I think inevitably that the fed just due to the, the, kind of the, the size of our,, of the us debt load,, the size of the Euro dollar system and just, and just, you know, the cost of kind of rolling this debt over in, and just the sheer size of the us entitlements,, and, and, you know, kind of fiscal obligations.

The Fed needs to, to monetize, the us debt, especially also, if we’re talking about dollar strength, the, the more that the dollar strengthens, the more that, again, that, that foreigners have to sell dollars, nominated assets of which the largest of those, those asset buckets is us treasuries is us debt.

Right? So, the more that the Fed tightens the paradox. The more that they’re gonna have to pick up the slack,, from, from, you know, kind of buying,, buying the U.S. debt because foreigners are selling it off to cover their, to cover their debt loads,, in dollars. Right? So the U.S. fiscal outlook, and the, and the debt burden is in, is in a worse spot the stronger that the dollar becomes.

So I think,, I’m kind of, of the opinion that the Fed will obviously pivot. If that wasn’t in implied already., but I think the end game here is, is yield curve control, similar to what,, the ECB and the BOJ are doing., whether that’s, you know, implicitly or explicitly,, you know, that the us is going to in some form and it’s gonna be some weird form of acronym, and it’s gonna be some, you know, obscure facility that may, that sounds super complicated in the Plex, but it’s gonna be some form of, of debt monetization, and it’s gonna be, you know, another form of money for, to Gober.

I think that’s, you know, when the case for Bitcoin., you know, an absolutely scarce monetary asset that’s, you know,, with no counterparty risk is, is going to, you know, once again,, once again, shine,, we’re not there yet, but I think that’s, that’s, what’s coming and you know, that could be six months, 12 months, 18 months. I really don’t know.

[00:46:43] Q: Or according to the,, chart, we were looking at the Euro dollar curve. It’ll probably reverse sometime around December of 2022 and start changing in 2023. But what do I know?, I want to go over open interest with you before I let you go back to doing what you do best,, slide 11.

And this is the middle., the middle of the top chart in particular, where you’ve shown an arrow pointing up., can you just touch on what you’re seeing, what you’re paying attention to here?

[00:47:15] Dylan: Yeah, I mean, we’ve, Bitcoin’s been in a range it’s like 22 5 to,, you know, I mean the, the lows were like 17 five, but,, you know, 19 18 5. Then in that range we’ve seen open interests, like sky rocket. So the lows were pretty, pretty heavily shorted., you can see that with the funding rate, but,, I’m kind of, I kind of expect whatever way equities go.,, Bitcoin is gonna kind of we’re, we’re consolidating in this range, but over the next say month or two,, equities are also kind of trading in a range, whatever way those go.

You see just such a massive buildup of open interest and again, like for every short there’s a long, so if there’s around, you know, 260, say 260,000 BTC worth of stable coin margin, open interest, those are just agreements to buy and sell, and you know, buyers and sellers meet. So there’s always an equal amount of shorts and longs.

But you know, if unlike spot Bitcoin where you can just lock Bitcoin away, cold storage and never sell it., open interest, you know, a derivative contract, a Fu futures contract., if you, if you buy a futures contract, you eventually have to sell it,, especially for like a perp, right? For a perpetual futures contract.

What we’re talking about in particular. And if you short, you eventually have to cover, there’s no way. You can say you could, you could short dollars, you know, by selling dollars for BTC, which is not technically shorting, but you could sell dollars for BTC and never cover. Right. But with a, with a derivative contract, you always have to exit your position.

So there’s just been a huge, like a huge build up of open interest. You’re just seeing like stablecoin margin, open interest, sort it to all time, high levels, especially as a percentage of, of market., and so I kind of expect over the next month or two,, while we’re still chopping around this range, right?

Like the range high is at 22, 5 22 6 today. Got, got invalidated pretty hard, whatever way equities go next. In my opinion, you’re, you’re gonna see a pretty VI,, violent move,, from BTC, whether that’s higher or lower,, because of just how much open interest has, has built up in this range over the last two months, a lot over the last.

This is obviously a more price action, technical talk., but that’s, that’s kind of what I gather from, from all this OI buildup is that whenever the, the true range is broken and it’s probably gonna be, you know, as a result of, of equity market,, or legacy market volatility,, I think that’s, you know, that’s where you see a massive move and it could be lower and it, you know, potentially could be higher as well, which would certainly not be a, not be a bad thing for, for us BTC holders, but that’s what I’m looking at.

[00:49:51] Q: All right. My final question for you is, are you actually bullish or bearish then?

[00:49:59] Dylan:, I mean, I’m, I’m long term bullish. I’m not, I’m not too bullish,, over the next, you know, whatever,, a couple weeks months,, maybe maybe quarter. So I still think there’s downside., I, I do have some cash. I, you know, mostly from shorting all coins over the last couple months here, but, I’m, I’m waiting to deploy that.

So, you know, if the lows are in great,, I gotta purchase in at 17 eight,, and we’re happy for that to be marked the bottom, but,, I think that, you know, we, we potentially have some more downside here, so.

[00:50:34] Q:, Dylan, it’s always a pleasure getting to hear your perspective. And of course,, nothing said here should be deemed as financial advice.

Everyone should be going and doing their own due diligence. If you listen to a couple talking heads online or on Twitter, you’re fucking idiot who deserves to get wrecked. I don’t make the rules. I just share them., Dylan, do you mind just sharing with everyone Bitcoin magazine pro I mean, we pretty much have gone over the latest issue you guys released on Friday.

Do you wanna just share a little bit more about maybe what you’re cooking up?

[00:51:05] Dylan: Yeah, sure., most of what we talked about today is, is kind of just running through,, previous issues of, of Bitcoin magazine pro, which is a Bitcoin focused newsletter, obviously by the name., but we, we like to cover,, all the, all the, kind of the, the.

Happenings in, in global macro,, in equity markets,, we cover Bitcoin matting,, with, with particular focus about once a week or so., so yeah, I mean, we, we, we put out free issues. We put out, we have a paid tier as well., but,, Sam and I,, Sam rule who’s, who’s out today,, with some family stuff, but,, we’re kind of the, the engine behind this and we have a great team supporting us.

Check that out. The Lincoln is in my bio,, but we’re putting. For the most part daily content, kind of around all this stuff. So if you, if you like to talk today, if you liked,,, what you saw, if you’re watching on YouTube, then, then give it a check out and appreciate everyone that tune.

[00:51:58] Q: I cannot stress how much signal comes out of this newsletter, how much I learn on a regular basis by subscribing there’s a free tier.

It costs you nothing., but your time and your time will be well spent by reading the words that Dylan and Sam and their team put together. So highly recommended. If you are not already subscribed to pop on over and subscribe to the free tier, it’ll start there., and of course, just a reminder to everyone listening, both on YouTube on Twitter,, Bitcoin Amsterdam is coming up.

Ticket prices will be going up on Friday, so be sure to lock it in. I am deep into the negotiations of trying to convince everyone at Bitcoin mag. Okay, cool. CKS outta the spaces. I am really trying hard to be able to smoke weed with you guys at Bitcoin Amsterdam. So buy your tickets and we’ll have a blast.

It’s gonna be the first. Bitcoin are the biggest Bitcoin conference in all of Europe, shoot us DMs with people you’d like to see talk, shoot us DMS with people or events or things that you’d like to see happen. There sound money Fest will be going on in Amsterdam of all places. Oh my God. I may never come back from that trip.

Lock in your tickets before ticket prices go up. And of course that’s a wrap P how’s that sound as a wrap. We good.

[00:53:15] P: Fantastic.

Let’s call it. We’ll see you all tomorrow. Same time, same place.

El Salvador’s Minister of the Economy Maria Luisa Hayem Brevé submitted a digital assets issuance bill to the country’s legislative assembly, paving the way for the launch of its bitcoin-backed “volcano” bonds.

First announced one year ago today, the pioneering initiative seeks to attract capital and investors to El Salvador. It was revealed at the time the plans to issue $1 billion in bonds on the Liquid Network, a federated Bitcoin sidechain, with the proceedings of the bonds being split between a $500 million direct allocation to bitcoin and an investment of the same amount in building out energy and bitcoin mining infrastructure in the region.

A sidechain is an independent blockchain that runs parallel to another blockchain, allowing for tokens from that blockchain to be used securely in the sidechain while abiding by a different set of rules, performance requirements, and security mechanisms. Liquid is a sidechain of Bitcoin that allows bitcoin to flow between the Liquid and Bitcoin networks with a two-way peg. A representation of bitcoin used in the Liquid network is referred to as L-BTC. Its verifiably equivalent amount of BTC is managed and secured by the network’s members, called functionaries.

“Digital securities law will enable El Salvador to be the financial center of central and south America,” wrote Paolo Ardoino, CTO of cryptocurrency exchange Bitfinex, on Twitter.

Bitfinex is set to be granted a license in order to be able to process and list the bond issuance in El Salvador.

The bonds will pay a 6.5% yield and enable fast-tracked citizenship for investors. The government will share half the additional gains with investors as a Bitcoin Dividend once the original $500 million has been monetized. These dividends will be dispersed annually using Blockstream’s asset management platform.

The act of submitting the bill, which was hinted at earlier this year, kickstarts the first major milestone before the bonds can see the light of day. The next is getting it approved, which is expected to happen before Christmas, a source close to President Nayib Bukele told Bitcoin Magazine. The bill was submitted on November 17 and presented to the country’s Congress today. It is embedded in full below.

This is an opinion editorial by Joakim Book, a Research Fellow at the American Institute for Economic Research, contributor and copy editor for Bitcoin Magazine and a writer on all things money and financial history.

I don’t.

That’s it. That’s the article.

In all sincerity, that is the full message: Just don’t do it. It’s not worth it.

You’re not an excited teenager anymore, in desperate need of bragging credits or trying out your newfound wisdom. You’re not a preaching priestess with lost souls to save right before some imminent arrival of the day of reckoning. We have time.

Instead: just leave people alone. Seriously. They came to Thanksgiving dinner to relax and rejoice with family, laugh, tell stories and zone out for a day — not to be ambushed with what to them will sound like a deranged rant in some obscure topic they couldn’t care less about. Even if it’s the monetary system, which nobody understands anyway.

Get real.

If you’re not convinced of this Dale Carnegie-esque social approach, and you still naively think that your meager words in between bites can change anybody’s view on anything, here are some more serious reasons for why you don’t talk to friends and family about Bitcoin the protocol — but most certainly not bitcoin, the asset:

- Your family and friends don’t want to hear it. Move on.

- For op-sec reasons, you don’t want to draw unnecessary attention to the fact that you probably have a decent bitcoin stack. Hopefully, family and close friends should be safe enough to confide in, but people talk and that gossip can only hurt you.

- People find bitcoin interesting only when they’re ready to; everyone gets the price they deserve. Like Gigi says in “21 Lessons:”

“Bitcoin will be understood by you as soon as you are ready, and I also believe that the first fractions of a bitcoin will find you as soon as you are ready to receive them. In essence, everyone will get ₿itcoin at exactly the right time.”

It’s highly unlikely that your uncle or mother-in-law just happens to be at that stage, just when you’re about to sit down for dinner.

- Unless you can claim youth, old age or extreme poverty, there are very few people who genuinely haven’t heard of bitcoin. That means your evangelizing wouldn’t be preaching to lost, ignorant souls ready to be saved but the tired, huddled and jaded masses who could care less about the discovery that will change their societies more than the internal combustion engine, internet and Big Government combined. Big deal.

- What is the case, however, is that everyone in your prospective audience has already had a couple of touchpoints and rejected bitcoin for this or that standard FUD. It’s a scam; seems weird; it’s dead; let’s trust the central bankers, who have our best interest at heart.

No amount of FUD busting changes that impression, because nobody holds uninformed and fringe convictions for rational reasons, reasons that can be flipped by your enthusiastic arguments in-between wiping off cranberry sauce and grabbing another turkey slice. - It really is bad form to talk about money — and bitcoin is the best money there is. Be classy.

Now, I’m not saying to never ever talk about Bitcoin. We love to talk Bitcoin — that’s why we go to meetups, join Twitter Spaces, write, code, run nodes, listen to podcasts, attend conferences. People there get something about this monetary rebellion and have opted in to be part of it. Your unsuspecting family members have not; ambushing them with the wonders of multisig, the magically fast Lightning transactions or how they too really need to get on this hype train, like, yesterday, is unlikely to go down well.

However, if in the post-dinner lull on the porch someone comes to you one-on-one, whisky in hand and of an inquisitive mind, that’s a very different story. That’s personal rather than public, and it’s without the time constraints that so usually trouble us. It involves clarifying questions or doubts for somebody who is both expressively curious about the topic and available for the talk. That’s rare — cherish it, and nurture it.

Last year I wrote something about the proper role of political conversations in social settings. Since November was also election month, it’s appropriate to cite here:

“Politics, I’m starting to believe, best belongs in the closet — rebranded and brought out for the specific occasion. Or perhaps the bedroom, with those you most trust, love, and respect. Not in public, not with strangers, not with friends, and most certainly not with other people in your community. Purge it from your being as much as you possibly could, and refuse to let political issues invade the areas of our lives that we cherish; politics and political disagreements don’t belong there, and our lives are too important to let them be ruled by (mostly contrived) political disagreements.”

If anything, those words seem more true today than they even did then. And I posit to you that the same applies for bitcoin.

Everyone has some sort of impression or opinion of bitcoin — and most of them are plain wrong. But there’s nothing people love more than a savior in white armor, riding in to dispel their errors about some thing they are freshly out of fucks for. Just like politics, nobody really cares.

Leave them alone. They will find bitcoin in their own time, just like all of us did.

This is a guest post by Joakim Book. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Federico Tenga, a long time contributor to Bitcoin projects with experience as start-up founder, consultant and educator.

The term “smart contracts” predates the invention of the blockchain and Bitcoin itself. Its first mention is in a 1994 article by Nick Szabo, who defined smart contracts as a “computerized transaction protocol that executes the terms of a contract.” While by this definition Bitcoin, thanks to its scripting language, supported smart contracts from the very first block, the term was popularized only later by Ethereum promoters, who twisted the original definition as “code that is redundantly executed by all nodes in a global consensus network”

While delegating code execution to a global consensus network has advantages (e.g. it is easy to deploy unowed contracts, such as the popularly automated market makers), this design has one major flaw: lack of scalability (and privacy). If every node in a network must redundantly run the same code, the amount of code that can actually be executed without excessively increasing the cost of running a node (and thus preserving decentralization) remains scarce, meaning that only a small number of contracts can be executed.

But what if we could design a system where the terms of the contract are executed and validated only by the parties involved, rather than by all members of the network? Let us imagine the example of a company that wants to issue shares. Instead of publishing the issuance contract publicly on a global ledger and using that ledger to track all future transfers of ownership, it could simply issue the shares privately and pass to the buyers the right to further transfer them. Then, the right to transfer ownership can be passed on to each new owner as if it were an amendment to the original issuance contract. In this way, each owner can independently verify that the shares he or she received are genuine by reading the original contract and validating that all the history of amendments that moved the shares conform to the rules set forth in the original contract.

This is actually nothing new, it is indeed the same mechanism that was used to transfer property before public registers became popular. In the U.K., for example, it was not compulsory to register a property when its ownership was transferred until the ‘90s. This means that still today over 15% of land in England and Wales is unregistered. If you are buying an unregistered property, instead of checking on a registry if the seller is the true owner, you would have to verify an unbroken chain of ownership going back at least 15 years (a period considered long enough to assume that the seller has sufficient title to the property). In doing so, you must ensure that any transfer of ownership has been carried out correctly and that any mortgages used for previous transactions have been paid off in full. This model has the advantage of improved privacy over ownership, and you do not have to rely on the maintainer of the public land register. On the other hand, it makes the verification of the seller’s ownership much more complicated for the buyer.

Source: Title deed of unregistered real estate propriety

How can the transfer of unregistered properties be improved? First of all, by making it a digitized process. If there is code that can be run by a computer to verify that all the history of ownership transfers is in compliance with the original contract rules, buying and selling becomes much faster and cheaper.

Secondly, to avoid the risk of the seller double-spending their asset, a system of proof of publication must be implemented. For example, we could implement a rule that every transfer of ownership must be committed on a predefined spot of a well-known newspaper (e.g. put the hash of the transfer of ownership in the upper-right corner of the first page of the New York Times). Since you cannot place the hash of a transfer in the same place twice, this prevents double-spending attempts. However, using a famous newspaper for this purpose has some disadvantages:

- You have to buy a lot of newspapers for the verification process. Not very practical.

- Each contract needs its own space in the newspaper. Not very scalable.

- The newspaper editor can easily censor or, even worse, simulate double-spending by putting a random hash in your slot, making any potential buyer of your asset think it has been sold before, and discouraging them from buying it. Not very trustless.

For these reasons, a better place to post proof of ownership transfers needs to be found. And what better option than the Bitcoin blockchain, an already established trusted public ledger with strong incentives to keep it censorship-resistant and decentralized?

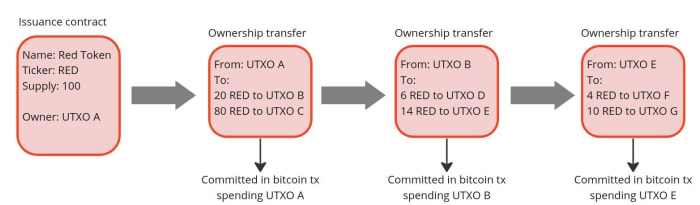

If we use Bitcoin, we should not specify a fixed place in the block where the commitment to transfer ownership must occur (e.g. in the first transaction) because, just like with the editor of the New York Times, the miner could mess with it. A better approach is to place the commitment in a predefined Bitcoin transaction, more specifically in a transaction that originates from an unspent transaction output (UTXO) to which the ownership of the asset to be issued is linked. The link between an asset and a bitcoin UTXO can occur either in the contract that issues the asset or in a subsequent transfer of ownership, each time making the target UTXO the controller of the transferred asset. In this way, we have clearly defined where the obligation to transfer ownership should be (i.e in the Bitcoin transaction originating from a particular UTXO). Anyone running a Bitcoin node can independently verify the commitments and neither the miners nor any other entity are able to censor or interfere with the asset transfer in any way.

Since on the Bitcoin blockchain we only publish a commitment of an ownership transfer, not the content of the transfer itself, the seller needs a dedicated communication channel to provide the buyer with all the proofs that the ownership transfer is valid. This could be done in a number of ways, potentially even by printing out the proofs and shipping them with a carrier pigeon, which, while a bit impractical, would still do the job. But the best option to avoid the censorship and privacy violations is establish a direct peer-to-peer encrypted communication, which compared to the pigeons also has the advantage of being easy to integrate with a software to verify the proofs received from the counterparty.

This model just described for client-side validated contracts and ownership transfers is exactly what has been implemented with the RGB protocol. With RGB, it is possible to create a contract that defines rights, assigns them to one or more existing bitcoin UTXO and specifies how their ownership can be transferred. The contract can be created starting from a template, called a “schema,” in which the creator of the contract only adjusts the parameters and ownership rights, as is done with traditional legal contracts. Currently, there are two types of schemas in RGB: one for issuing fungible tokens (RGB20) and a second for issuing collectibles (RGB21), but in the future, more schemas can be developed by anyone in a permissionless fashion without requiring changes at the protocol level.

To use a more practical example, an issuer of fungible assets (e.g. company shares, stablecoins, etc.) can use the RGB20 schema template and create a contract defining how many tokens it will issue, the name of the asset and some additional metadata associated with it. It can then define which bitcoin UTXO has the right to transfer ownership of the created tokens and assign other rights to other UTXOs, such as the right to make a secondary issuance or to renominate the asset. Each client receiving tokens created by this contract will be able to verify the content of the Genesis contract and validate that any transfer of ownership in the history of the token received has complied with the rules set out therein.

So what can we do with RGB in practice today? First and foremost, it enables the issuance and the transfer of tokenized assets with better scalability and privacy compared to any existing alternative. On the privacy side, RGB benefits from the fact that all transfer-related data is kept client-side, so a blockchain observer cannot extract any information about the user’s financial activities (it is not even possible to distinguish a bitcoin transaction containing an RGB commitment from a regular one), moreover, the receiver shares with the sender only blinded UTXO (i. e. the hash of the concatenation between the UTXO in which she wish to receive the assets and a random number) instead of the UTXO itself, so it is not possible for the payer to monitor future activities of the receiver. To further increase the privacy of users, RGB also adopts the bulletproof cryptographic mechanism to hide the amounts in the history of asset transfers, so that even future owners of assets have an obfuscated view of the financial behavior of previous holders.

In terms of scalability, RGB offers some advantages as well. First of all, most of the data is kept off-chain, as the blockchain is only used as a commitment layer, reducing the fees that need to be paid and meaning that each client only validates the transfers it is interested in instead of all the activity of a global network. Since an RGB transfer still requires a Bitcoin transaction, the fee saving may seem minimal, but when you start introducing transaction batching they can quickly become massive. Indeed, it is possible to transfer all the tokens (or, more generally, “rights”) associated with a UTXO towards an arbitrary amount of recipients with a single commitment in a single bitcoin transaction. Let’s assume you are a service provider making payouts to several users at once. With RGB, you can commit in a single Bitcoin transaction thousands of transfers to thousands of users requesting different types of assets, making the marginal cost of each single payout absolutely negligible.

Another fee-saving mechanism for issuers of low value assets is that in RGB the issuance of an asset does not require paying fees. This happens because the creation of an issuance contract does not need to be committed on the blockchain. A contract simply defines to which already existing UTXO the newly issued assets will be allocated to. So if you are an artist interested in creating collectible tokens, you can issue as many as you want for free and then only pay the bitcoin transaction fee when a buyer shows up and requests the token to be assigned to their UTXO.

Furthermore, because RGB is built on top of bitcoin transactions, it is also compatible with the Lightning Network. While it is not yet implemented at the time of writing, it will be possible to create asset-specific Lightning channels and route payments through them, similar to how it works with normal Lightning transactions.

Conclusion

RGB is a groundbreaking innovation that opens up to new use cases using a completely new paradigm, but which tools are available to use it? If you want to experiment with the core of the technology itself, you should directly try out the RGB node. If you want to build applications on top of RGB without having to deep dive into the complexity of the protocol, you can use the rgb-lib library, which provides a simple interface for developers. If you just want to try to issue and transfer assets, you can play with Iris Wallet for Android, whose code is also open source on GitHub. If you just want to learn more about RGB you can check out this list of resources.

This is a guest post by Federico Tenga. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.